While Western malls face decline, India’s retail sector is booming, attracting significant global investment. This surprising trend, highlighted by real estate consultancy Anarock, positions Indian malls as a key growth area in a world increasingly dominated by e-commerce and shifting consumer habits. The resilience of the Indian market is a stark contrast to the struggles seen in the US and Europe, making it a focal point for international brands and investors.

The Global Mall Crisis and India’s Divergent Path

The retail landscape is undergoing a dramatic transformation globally. In the United States, a net closure of nearly 1,200 mall stores since 2020 paints a grim picture. Rising vacancies are forcing a significant number of malls – almost 40% – to undergo costly and often disruptive rezoning or repurposing. This “retail apocalypse,” fueled by the rise of online shopping and changing consumer preferences, has left many Western developers scrambling to adapt.

However, India is bucking this trend. Instead of decline, the country is experiencing a genuine retail resurgence. Anarock reports that Indian malls are poised to receive over USD 3.5 billion in capital inflows over the next three years, a testament to the confidence investors have in the market’s potential. This influx is driven by a potent combination of factors, including strong consumer demand, a burgeoning middle class, and supportive government policies.

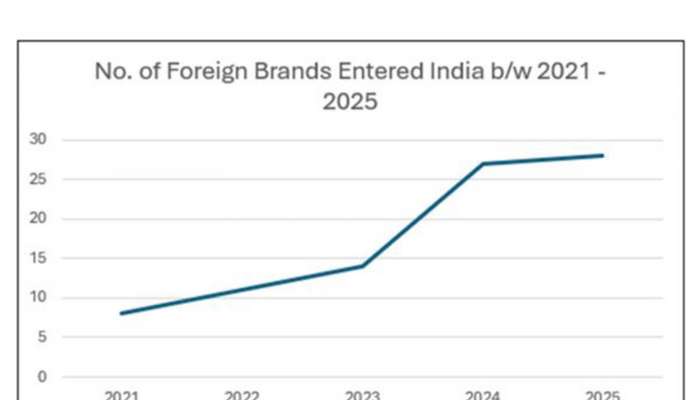

A Flood of International Brands

The appeal of the Indian market is evident in the growing number of foreign brands establishing a presence. Anarock notes that over 88 international brands have entered Indian retail recently, and are actively seeking expansion opportunities. Many more are in the pipeline, eager to secure space in the limited number of high-quality, Grade-A malls currently available. This demand is creating a competitive environment and driving up property values.

Why Indian Malls Are Thriving: Key Drivers

Several unique characteristics are contributing to the success of Indian malls. Unlike their Western counterparts, they aren’t simply shopping centers; they’ve evolved into comprehensive lifestyle destinations.

Unmet Demand and Limited Organized Retail

A primary driver of this growth is the significant undersupply of quality retail space in India. Per capita retail stock remains remarkably low compared to developed markets like the US and China. This scarcity, coupled with a rapidly increasing per capita income – nearly doubling in the last decade – has created a substantial demand-supply imbalance.

This gap isn’t just about quantity; it’s about quality. Consumers are increasingly seeking the curated experiences and brand variety offered by modern, well-managed malls. This preference is particularly strong among India’s young and growing population.

The Resilience of Experiential Retail

Indian malls have successfully integrated entertainment, dining, and social experiences into their offerings. Foot traffic in major malls consistently exceeds 20,000 on weekdays and surges past 40,000 on weekends. Food and beverage (F&B) and entertainment options now account for 30-35% of this footfall, creating a resilient retail mix that is less vulnerable to the disruptions caused by e-commerce.

This focus on experience is a key differentiator. While online shopping offers convenience, it cannot replicate the social and sensory aspects of visiting a mall – a crucial element for many Indian consumers. The mall becomes a place to spend time with family and friends, enjoy a meal, catch a movie, and discover new products.

E-commerce as a Complement, Not a Competitor

Interestingly, Indian malls aren’t being undermined by e-commerce; they are, in many ways, benefiting from it. Despite rapid growth, e-commerce penetration in India remains relatively low, around 8%, compared to over 20% in both China and the US.

This suggests that a significant portion of the Indian population still prefers the traditional brick-and-mortar shopping experience. Furthermore, many brands are using physical stores in malls to complement their online presence, offering customers a chance to see and try products before purchasing. This omnichannel approach is proving to be highly effective. The rise of quick commerce is also driving footfall as consumers use malls as pick-up points.

The Future of Indian Retail and Investment Opportunities

Anarock predicts that India is on track to become a USD 6 trillion consumption economy by 2030, further solidifying its position as a global retail hotspot. The consistent high occupancy rates in Grade-A malls – typically 95-100% with substantial waitlists – demonstrate the strong demand for quality retail space. Rental growth is also consistently exceeding pre-pandemic levels, and developers are finding that leasing cycles are outpacing construction cycles, a rare phenomenon in the global retail market.

This positive outlook is attracting significant investment, not just from foreign brands but also from institutional investors. The combination of demographic advantages, increasing disposable incomes, and a relatively underdeveloped retail infrastructure makes India a compelling investment destination. The focus on creating experiential destinations within Indian malls is expected to continue, further enhancing their appeal to consumers and driving growth in the sector.

In conclusion, while the future of retail in many Western countries remains uncertain, India presents a compelling counter-narrative. The country’s unique market dynamics, coupled with strong economic fundamentals, are creating a thriving retail ecosystem that is attracting global capital and redefining the role of the modern mall. Investors and brands looking for growth opportunities in the retail sector should seriously consider the potential of the Indian market.