Starting on September 1st, all licensed financial and banking institutions in Bahrain must comply with new “open banking” regulations set forth by the Central Bank of Bahrain (CBB). These regulations include obtaining customer consent and authentication, licensee disclosures, and reporting on the performance of application programming interfaces (APIs) by service providers. A recent circular issued by Khalid Humaidan, Governor of the CBB, outlined these requirements, which also include providing information to payment service providers about legal entities after obtaining their consent.

The circular also introduced amendments to extend open banking services to legal entities such as institutions and companies, impacting the General Requirements Module in the CBB’s Guidebook Volumes 1 and 2, as well as the Open Banking Module in Volume 5. This means that customer account data requirements must be detailed by information and payment service providers for any use cases related to account information. Changes to the Reporting Requirements Module and the Public Disclosure Requirements Module within Volumes 1 and 2 were also introduced, focusing on the disclosure of API performance by account service providers.

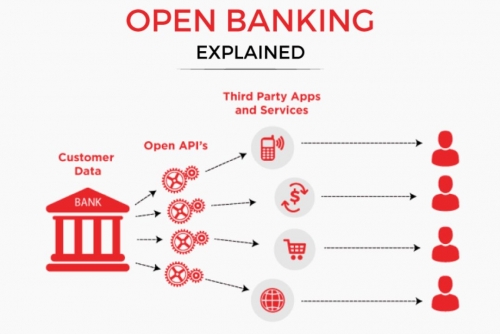

Guidance on business models for information and payment service providers will be included in the open banking module of the CBB’s Guidebook, Volume 5. Licensed banks are required to work with Benefit Company to implement the “integrated cash flow” model, which involves obtaining initial customer consent and authentication during the onboarding process. Information and payment service providers must also agree with banks on standard API specifications and service standards aligned with security guidelines under Bahrain’s Open Banking framework.

These amendments follow consultations initiated by the CBB in March and October 2023, and all licensed financial and banking institutions must submit an action plan by June 30th of the previous year. Open banking is expected to encourage Bahraini financial technology companies to develop new financial products and services, such as budgeting applications, personal loan offers, and investment platforms, by leveraging open banking data. This move towards open banking is aimed at promoting innovation and competition within Bahrain’s financial sector.

In conclusion, it is important for financial and banking institutions in Bahrain to adhere to the new open banking regulations starting on September 1st. These regulations include obtaining customer consent and authentication, licensee disclosures, and reporting on API performance by service providers. By extending open banking services to legal entities, such as institutions and companies, the CBB aims to promote innovation and competition within the financial sector. This shift towards open banking is expected to encourage the development of new financial products and services by Bahraini financial technology companies, ultimately benefiting consumers and businesses in the region.